Last week GameStop went viral as a topic unlike anything I’d seen in my 10 years at Human Investing. Probably just like you, I googled “Gamma Squeeze”, had someone two degrees of separation from me divulge they had been a part of wallstreetbets, and now have significantly more money, and felt like I was watching a version of March Madness play out real-time in the financial markets.

With the introduction of free trading and the gamification of trading stocks with apps like Robinhood, this past week was the culmination of many factors colliding (more on that later). Different than in The Big Short (2008 Real Estate Crisis) where select hedge funds were taking advantage of large investment banks being overleveraged in the housing market, this time it was retail investors taking advantage of hedge funds overleveraged in GameStop. If Michael Lewis or someone else isn‘t writing this book already I’d be shocked, and I can’t wait for the movie too.

Most of the questions our team has been fielding this week looked like a version of:

Why GameStop?

Why now?

Is this a one-time occurrence or is something like this going to be happening more frequently?

And probably most importantly what does this mean for me, my investments, and the markets as a whole?

To help me answer some of these questions I’ve enlisted our head analyst, Andrew Gladhill. In our office known as Glads. For those of you who haven’t spoken with Glads or seen his work, he’s a CFA and anyone who knows him would most likely have him on their Who Wants to be Millionaire “phone a friend” shortlist. Maybe most importantly, one of the ways Glads makes our team better is being able to take complex topics and break them down in very digestible terms. Take it away!

Some key terms you need to know

Shorting

The short answer: Shorting is betting that a price will go down (not up), and you benefit as the price goes down. For example, if you short a stock trading at $20, and it goes down to $15, you have made $5.

The long answer: Shorting works through a few steps:

Step 1 – you borrow the stock today from someone who holds the stock (Let’s call them Emily) with a set date you must return the stock back to Emily. Emily lends you the stock because Emily charges you interest.

Step 2 – you sell the stock today (say for $20)

Step 3 – you must return the stock to Emily, plus interest (say $1) buying it at the current market price to do so (say $15)

In this example, you have made $4 (Sold for $20, bought for $15, charged $1 interest)

Why do you short? Because you believe something is overvalued, and you want to profit from when the price goes down.

Short Squeeze

The short answer: When a shorted position has the price increase, those who are shorting it (the shorters) are forced to buy the position, driving the price up further.

The long answer: If the price rises on a short position, the shorter starts losing money. They can either hedge their losses by buying the stock before the return date, or wait to buy and hope the price falls. Remember, the shorter must return the stock to the original owner by a set deadline. Because the price of the stock can rise higher and higher, the shorter’s potential loss is limitless.

So a short squeeze is when the price of a company goes up because lots of people are buying a heavily shorted stock, increasing the price. The rise in price causes some shorters to close out their positions, which involves buying the stock. More buying activity causes the price to increase, causing greater losses for the shorters. If the price rises high enough, the losses get large enough that more shorters are forced to close out their short position to avoid having their total portfolio value go negative. This creates a positive feedback cycle of buying activity, pushing the stock price even higher.

Why WAS Gamestop ($GME) TARGETED?

The Short answer: GME had an unusually high amount of shares sold short, allowing the short squeeze to be possible. Retail investors gathered online & decided to try to make it happen.

The Long Answer: Short float is the number of shares sold short (borrowed & then sold) that have not yet been repurchased. Gamestop had a short float over 100%, meaning some shares of Gamestop had been lent out more than once. This happened because many believed Gamestop (a retail video game store) was the next Blockbuster and would go out of business. The share price would go to $0 a share, and they would profit from the price dropping. Some retail investors noticed the high short float on GME in an online community known as reddit wallstreetbets (aka WSB, aka retail investors). The retail investors saw an opportunity for a short squeeze due to the large short interest, and GME being a relatively small company.

The retail investors planned to force a short squeeze on GME. The retail investors would buy up as many shares of GME as possible, driving up the price. The retail investors would hold their shares, drying up the supply, pushing the price up even further. All this upward price movement would force a short squeeze, driving the price up even further, and the positive feedback cycle would result in astronomical price increases for GME as the short squeeze hits. Retail investors will be able to sell their shares at high prices to the shorters forced to closing out their position.

Why was trading restricted?

The short answer: Companies that execute trades (brokerages, i.e. Robinhood) must have money to cover trade differences with clearing firms (the back end companies that finalize trades) as collateral. The rapid, unexpected movement in GME brought some brokerages ability to do that into question, and they had to pause the trading until they could secure more funding.

The long answer: When you sell or purchase a stock, that trade isn’t finalized until settlement, which is 2 days later. This time is used to verify the transfer of cash & the security purchased. It’s like when you deposit a check at the bank, the bank makes sure the check clears before you can withdraw cash. Clearing firms finalize stock transactions. The brokerages (i.e. Robinhood, Fidelity, Schwab, e-Trade) are required by law to maintain cash deposits as collateral with clearing firms to cover any losses. The required deposits by the clearing firms for the brokerages went up because GME was having higher price volatility. Some brokerages had to pause trading in GME while they secured enough funding to make the deposits required by the clearing firms. The financial system rarely handles meteoric rises in stock prices in such a short amount of time, and certain parts of the system that normally work so smoothly we never think about them suddenly brought trading to a screeching halt.

what does this mean for me and my portfolio?

Thank you, Glads. This story and its ramifications are certainly not finished. As more details come out it will continue to paint a clearer picture of what it means for investors over the past week and looking forward as well. To bring this all home and answer the question, “what does this mean for me and my portfolio” a few thoughts:

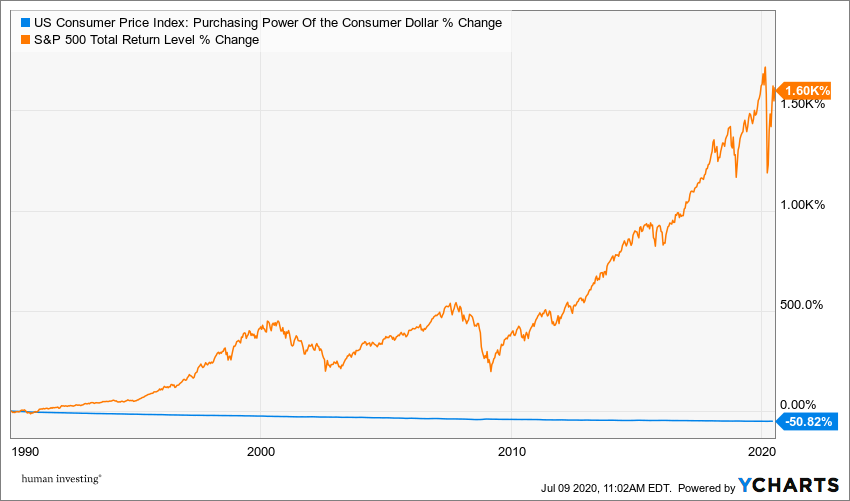

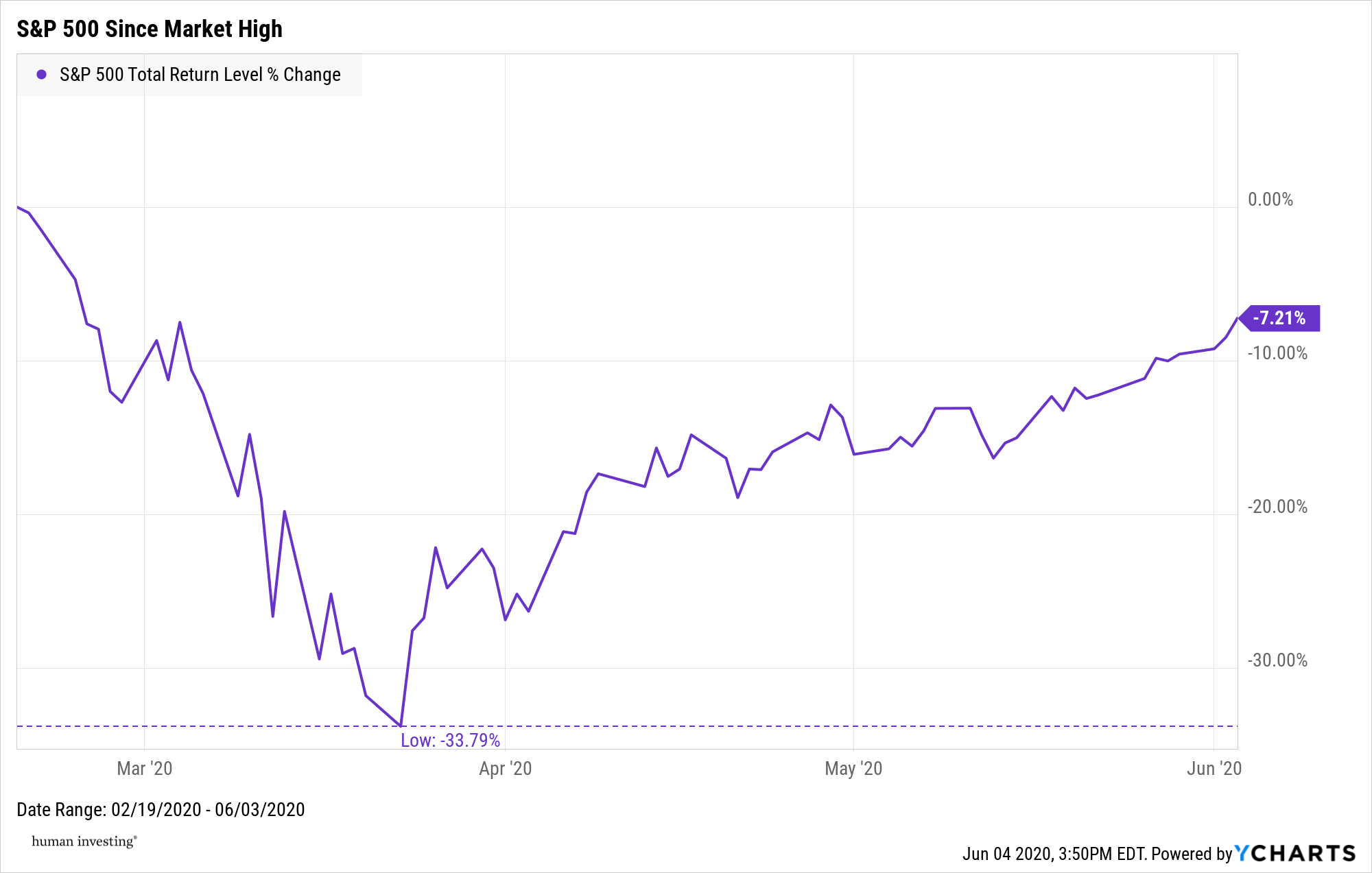

While Gamestop took up all the headlines this past week, for most investors it had little to no impact on their portfolio. For example, the Vanguard Total Stock Market Fund (VTI), is a staple in many retirement accounts across the country, the fund was down 3.59% last week (in line with the market). GameStop contributed a positive 0.04% return to the fund (basically nothing!) despite being up nearly 655% on the week, a bi-product of how small of a company GameStop is relative to other companies in the fund that truly move the needle.

So should I get in?

Should you open up a trading account in preparation of the next public short-squeeze? The boring/correct answer is this is not the forum to be giving specific financial advice for your specific situation. If you’re truly speculating about that and want to talk to it through, PLEASE sign up for a Calendly link with one of our advisors and they are happy to talk with you about it.

My favorite book I’ve read in the past few months is The Psychology of Money by Morgan Housel. It’s one of the best (in my opinion) personal finance books because it focuses on behavior (potential controllable actions) rather than guessing what’s the next best stock is. He has an entire chapter devoted to the topic of, “People have a tendency to be influenced by the actions of other people who are playing a different financial game than they are.” This is the case for most people saving for retirement when thinking about GameStop, shorting, and what we’ve seen in the news. It’s Human to feel like you missed on an opportunity with GameStop and to want to hit it big on the next trade. But most likely that’s not your game. Most likely your game (and mine too) involves saving and investing for a long time, letting compounding interest take care of the rest, and maybe most importantly staying out of your own way. And while that game doesn’t create the same headlines, as Housel writes in a different chapter it can create a different type of headline to aspire to.

Related Articles